4.7

Owner's of the HP (Hewlett-Packard) Calculator HP 12C Financial Calculator gave it a score of 4.7 out of 5. Here's how the scores stacked up:

44 Section 3: Basic Financial Functions

File name: hp 12c pt_user's guide_English_HDPMF123E27 Page: 44 of 275

Printed Date: 2005/8/1 Dimension: 14.8 cm x 21 cm

Financial Calculations and the Cash Flow Diagram

The concepts and examples presented in this section are representative of a wide

range of financial calculations. If your specific problem does not appear to be

illustrated in the pages that follow, don’t assume that the calculator is not capable

of solving it. Every financial calculation involves certain basic elements; but the

terminology used to refer to these elements typically differs among the various

segments of the business and financial communities. All you need to do is identify

the basic elements in your problem, and then structure the problem so that it will

be readily apparent what quantities you need to tell the calculator and what

quantity you want to solve for.

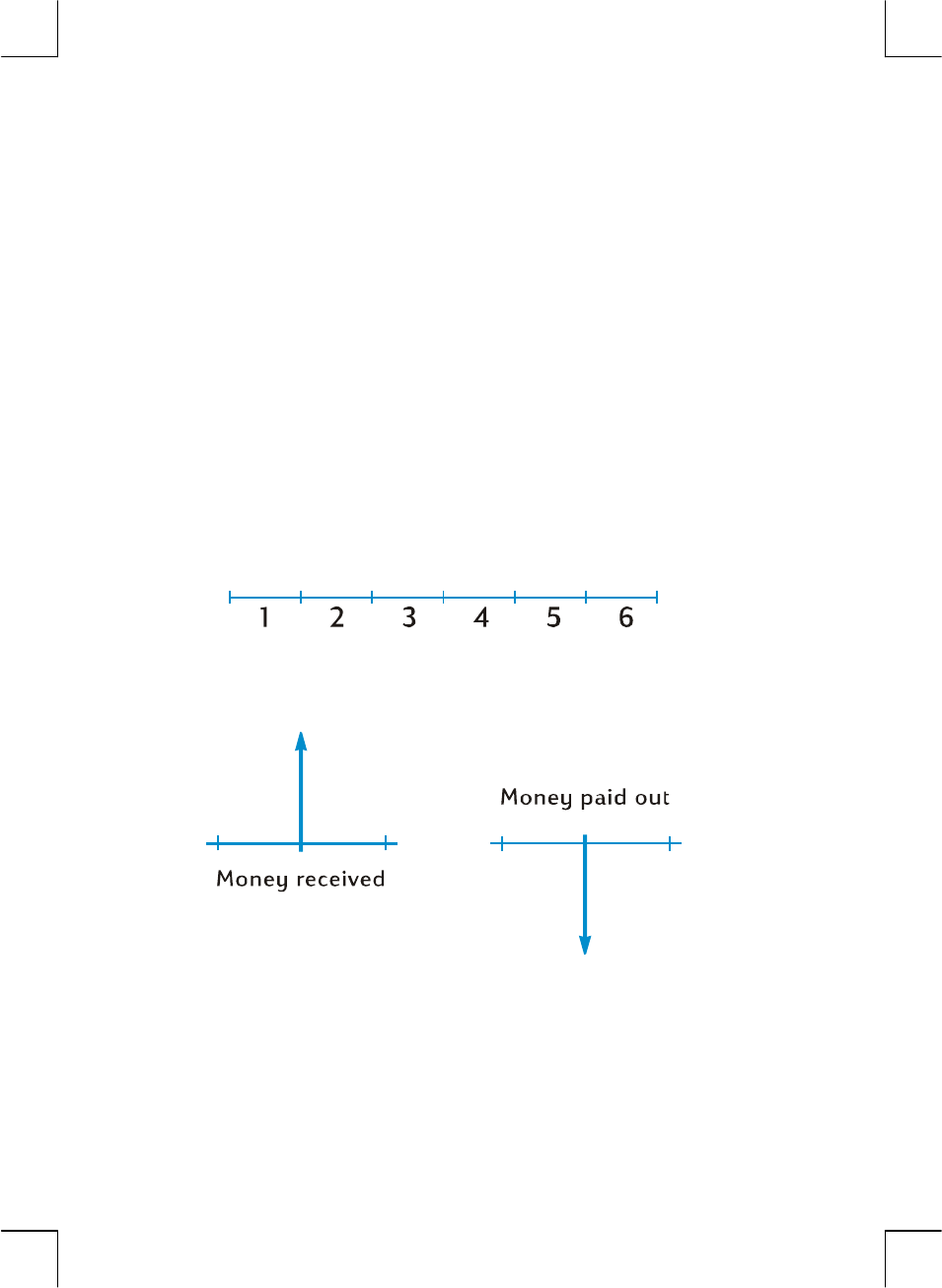

An invaluable aid for using your calculator in a financial calculation is the cash

flow diagram. This is simply a pictorial representation of the timing and direction

of financial transactions, labeled in terms that correspond to keys on the calculator.

The diagram begins with a horizontal line, called a time line. It represents the

duration of a financial problem, and is divided into compounding periods. For

example, a financial problem that transpires over 6 months with monthly

compounding would be diagrammed like this:

The exchange of money in a problem is depicted by vertical arrows. Money you

receive is represented by an arrow pointing up from the point in the time line when

the transaction occurs; money you pay out is represented by an arrow pointing

down.

Suppose you deposited (paid out) $1,000 into an account that pays 6% annual

interest and is compounded monthly, and you subsequently deposited an

additional $50 at the end of each month for the next 2 years. The cash flow

diagram describing the problem would look like this:

Find Your Products By Category

- Computer Equipment

- Portable Media

- Photography

- Car Audio and Video

- TV and Video

- Household Appliance

- Automotive

- Communications

- Kitchen Appliance

- Laundry Appliance

- Home Audio

- Lawn and Garden

- Power Tools

- Musical Instruments & Equipment

- Baby

- Personal Care

- Video Game

- Marine Equipment

- Fitness & Sports

- Outdoor Cooking

- Cell Phone

Please Login